Widgetized Section

Go to Admin » Appearance » Widgets » and move Gabfire Widget: Social into that MastheadOverlay zone

Are We in a Recession? The Shutdown Makes It Harder to Know

The views expressed are those of the author and do not necessarily reflect the views of ASPA as an organization.

By Ben Tafoya

December 5, 2025

The federal government shutdown we just experienced created an unusual problem: determining whether we’re in a recession or the general state of the economy is now more difficult precisely because of the shutdown itself. The lack of data confuses the public and policymakers alike. October 2025’s economic data including critical inflation and employment reports may never be released, leaving what experts call “a permanent blind spot in America’s official record.” Federal workers who would have collected Consumer Price Index data weren’t deployed after October 1, making that month’s inflation report unlikely to ever publish.

Understanding What Defines a Recession

A recession is traditionally defined as two consecutive quarters of negative economic growth measured by Gross Domestic Product. However, the National Bureau of Economic Research, which officially declares recessions, considers multiple factors: employment levels, personal income, manufacturing output and consumer spending.

The challenge is timing. The Q3 report was due at the end of October but was not completed. The Q4 GDP report isn’t scheduled until January 30, 2026 and could be delayed further due to missing October data. We won’t have definitive answers on the recession question for months.

What the Available Data Shows

The Institute for Supply Management (ISM) Manufacturing Index fell to 48.7 in October, marking the eighth consecutive month of contraction. Any reading below 50 indicates economic decline. Manufacturing respondents frequently cited tariffs as causing substantial struggles, reporting added costs, price volatility and challenges with reshoring production. Businesses described conditions as “severely depressed.”

The services sector, which covers the vast majority of the US economy, showed more resilience. The ISM Services Index registered 52.4 in October, up from 50.0 in September and reaching an eight-month high. Business activity and new orders increased substantially.

However, the employment component remained in contraction for a fifth straight month. Some respondents pointed to disruptions from both tariffs and the shutdown, with industries exposed to the public sector seeing negative impacts.

Without official Bureau of Labor Statistics data on employment, private firms filled the gap. ADP reported 143,000 private-sector jobs added in September but noted a “significant decline in hiring momentum throughout the year,” describing conditions as “a low-hire, even a no-hire, and low-fire economy.” The delayed BLS report showed the same type of job growth but a higher unemployment rate. Weekly unemployment claims, reconstructed by Goldman Sachs using state data, remained at historically low levels around 224,000. Companies have begun mass layoffs but it is not clear how long or deep these changes will be.

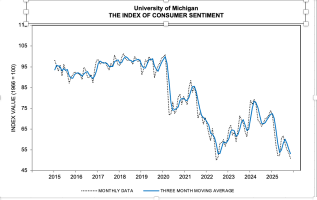

The University of Michigan’s consumer sentiment index plunged to 50.3 in November, its lowest level since June 2022 and the second-lowest reading in the survey’s history dating back to 1978. This represents a 30% decline from a year earlier. One notable exception: consumers with large stock holdings saw sentiment increase 11% supported by continued stock market strength. This highlights what economists call a “K-shaped economy” where higher-income households continue doing well while lower-income Americans perceive struggle.

The shutdown itself became a significant economic factor. The Congressional Budget Office estimated the six-week closure would reduce Q4 growth by about 1.5 percentage points. About $11 billion in economic activity will be permanently lost. The ripple effects extended beyond federal paychecks. Eight billion dollars in SNAP food aid to 42 million recipients was delayed, likely reducing consumer spending. Tourism spending fell by $63 million per day—an estimated $2.6 billion over six weeks. While federal workers will receive back pay, the economic drag from delayed spending has already occurred and won’t be fully recovered.

The missing data has complicated Federal Reserve decision-making. Fed Chair Jerome Powell described the situation memorably: “What do you do if you’re driving in the fog? You slow down.” He suggested the central bank might pause interest rate cuts due to insufficient information potentially keeping borrowing costs higher for longer.

The Bottom Line: Slowdown

Most available evidence suggests a significant economic slowdown rather than a full-blown recession.

Evidence against recession: Unemployment remains historically low. The services sector continues modest growth. Consumer balance sheets remain relatively strong with disposable income and wages growing steadily enough to sustain spending particularly among higher-income households.

Evidence of weakness: Manufacturing has been contracting for eight consecutive months. Hiring momentum is declining substantially. Consumer confidence sits at near-record lows. The shutdown created measurable, permanent economic damage. Polls show broad dissatisfaction with the state of the economy.

The honest answer: We’re experiencing an economy weakened by policy uncertainty, tariff disruptions and the shutdown itself not a traditional recession driven by financial crisis or collapsing consumer demand. The technical determination won’t be possible until 2026 when complete fourth-quarter data is analyzed.

For government employees wondering about job security and economic stability, the current situation appears to be one of frustration and stagnation rather than catastrophe. The economy is clearly limping but not collapsing. State revenues will provide a clue and there are warning signs there too. But the full picture won’t be clear for months and the missing data from the shutdown will leave permanent gaps in our understanding of this period.

Author: Dr. Ben Tafoya, a retired public administrator, is an adjunct faculty member teaching economics at Northeastern University in Boston. Ben is the author of a chapter on social equity and public Administration in the volume from Birkdale, Public Affairs Practicum. He can be reached at [email protected] or on BlueSky @PolicyBen. All opinions and mistakes are his alone.

(1 votes, average: 5.00 out of 5)

(1 votes, average: 5.00 out of 5)![]() Loading...

Loading...

Follow Us!