Widgetized Section

Go to Admin » Appearance » Widgets » and move Gabfire Widget: Social into that MastheadOverlay zone

Legitimacy-Capacity Discrepancy to Create Public Value

The views expressed are those of the author and do not necessarily reflect the views of ASPA as an organization.

By Md Eyasin Ul Islam Pavel

May 1, 2026

External Mandates and the Burden of Implementation

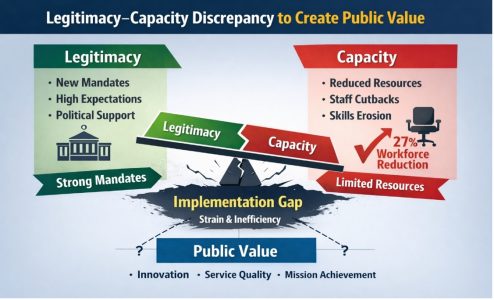

The Internal Revenue Service (IRS) currently stands as an involuntary laboratory for a profound experiment in American governance. As the 2026 tax season begins, the agency is facing two major pressures at the same time. On one side, the IRS is facing new operational demands from recent policy changes, especially from the “One Big Beautiful Bill” (OBBB) Act, which requires the IRS to process more than 100 tax adjustments. The OBBBA introduced new rules for tips and overtime income and created a new “Trump Account” pilot program for child savings. These changes have significantly increased the agency’s responsibilities.

At the same time, the 2025 National Taxpayer Advocate report shows the agency lost 27 percent of its total workforce. More than 26,000 employees left in 2025 through buyouts and reductions in force. This situation has created a clear gap between what the IRS is expected to do and what it can actually deliver. As a result, its capacity to create public value is weakening.

Mark H. Moore defines public value as the benefits created by public organizations, including innovation, service quality and mission achievement. This challenge is not limited to the IRS. It reflects a broader issue across public administration. Many government agencies are facing similar tensions. The key question is how the gap between growing policy-mandated responsibilities and declining capacity can be addressed.

The Technological Paradox and the Human Element

Administrations have often pointed to an “AI boom” as a solution to staffing gaps, suggesting that automation can bridge the legitimacy–capacity divide. However, the Government Accountability Office has warned that the loss of 25 percent of the IRS’s IT and data science staff has left the agency without sufficient “human-in-the-loop” capacity to safely deploy or monitor these systems.

Artificial intelligence requires clean data and expert oversight to function effectively in a regulatory environment. Without sufficient human capital to manage implementation, the push for technological efficiency risks becoming another operational burden. The result is a “digital backlog.” Automated systems flag millions of tax returns for review, but there are not enough staff to process them. As a result, both procedural legitimacy and operational capacity are strained.

Shifting Paradigms: From Expertise to Loyalty

This discrepancy is not unique to tax administration; it reflects a broader shift in public administration paradigms. For decades, the field moved from Old Public Administration (OPA), with its emphasis on neutral hierarchy, to New Public Management (NPM) and its focus on efficiency and market-like competition. More recently, New Public Governance (NPG) has emphasized collaborative, network-based value and the role of civil servants as stewards of the public interest.

Today, however, developments such as Schedule Policy/Career signal a shift toward politicized managerialism that challenges established administrative frameworks. This approach prioritizes political responsiveness, a form of external legitimacy, over procedural legitimacy and technical capacity. In this environment, performance is increasingly measured by how quickly agencies implement policy agendas rather than by service quality or mission achievement.

The Theoretical Conflict of the Strategic Triangle

In public value theory, Mark Moore’s Strategic Triangle suggests that effective public organizations require three elements: legitimate and supported goals, sufficient operational capacity and meaningful public outcomes.

The current environment shows increasing strain across this balance. Agencies may receive strong mandates, but operational capacity does not always keep pace. When this occurs, the triangle becomes misaligned, weakening the ability of agencies to deliver public value in practice.

A Way Out of the Legitimacy–Capacity Discrepancy

To address this challenge, the IRS and other agencies must move beyond compliance with external mandates and reinvest in human capital capacity. While Mark Moore emphasizes the importance of public value creation, this article highlights the merit principle as a key mechanism for enabling that value in practice.

Merit principles protect qualified employees from arbitrary displacement and help preserve institutional knowledge. Without stable and experienced staff to translate complex law into implementation, mandates remain legitimate in theory but ineffective in practice.

Policies provide democratic legitimacy and authorize government action, while the merit principle supports procedural legitimacy and ensures that action is carried out competently and fairly. By hiring and retaining employees based on knowledge, skills and abilities rather than political loyalty, agencies can strengthen both capacity and implementation effectiveness.

In sum, reinforcing the merit principle is essential to restoring the balance between legitimacy and capacity and ensuring that policy mandates translate into meaningful public value.

Author: Md Eyasin Ul Islam Pavel is a PhD student in Public Affairs at the University of Texas at Dallas.

(No Ratings Yet)

(No Ratings Yet)![]() Loading...

Loading...

Follow Us!