Widgetized Section

Go to Admin » Appearance » Widgets » and move Gabfire Widget: Social into that MastheadOverlay zone

How to Turn the Budget into a Good Management Tool

By Scott Lazenby

http://3.bp.blogspot.com

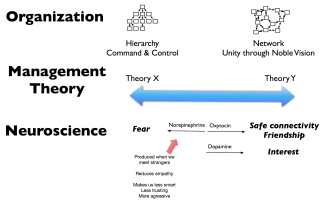

Decades of research have confirmed the importance of delegating both authority and responsibility, of empowering employees, and of ensuring that staff members have the resources they need to get the job done. To use Douglas McGregor’s Theory X and Theory Y labels, budget systems typically used by governments are built on a Theory X philosophy, in which operating managers are assumed to be lazy and stupid (or conniving), they avoid responsibility, and prefer to be directed (preferably by OMB directors or central budget analysts).

A handful of governments, however, have experimented with budget management systems that are based on Theory Y principles, which assume that employees can in fact exercise self-direction and self-control, and they willingly accept responsibility. Osborne and Gaebler, in Reinventing Government, introduced some of the elements of these systems (a bottom-line focus, and carryover savings), described as “expenditure control budgeting.”

Based on my experience of over three decades managing cities, and managing and studying budget systems, I would propose the following elements of a full “Theory Y” budget management system:

- A clear definition of objectives and expected service outcomes. For local governments, these are defined by the governing body, with citizens involved in setting overall values and priorities. At the state and national levels, they are typically set by the elected CEO and agency directors.

- Setting limits, or as Osborne and Hutchinson put it, establishing the price of government. At the organizational level, these come in the form of rates for taxes, permits, and user fees. For programs within the general fund, they come in the form of a set allocation of general revenues. This is similar to the concept of target-based budgeting.

- Allocating departmental revenues directly to the associated departments, rather than lumped in a general fund revenue account.

- Holding managers responsible for the bottom line, giving them full freedom to shift resources between line items or categories of expense.

- Holding managers accountable for the outcomes expected of them (see step 1).

- Allowing operating units to carry forward 100% of bottom-line savings into the next fiscal year.

Decentralizing management of both revenues and expenditures allows the organization to respond quickly and (almost) automatically to changes in the financial environment (revenue gains or shortfalls, unexpected expenses). It therefore becomes possible to extend the budget period to twenty-four months or longer. A side benefit is a significant savings in time spent on the budget by staff and the governing body.

If this sounds good in principle (and I hope it does), the reader who has experienced traditional governmental (or large corporate) budget systems may wonder, “What does a budget prepared under this system actually look like?” Stay tuned…

(5 votes, average: 2.60 out of 5)

(5 votes, average: 2.60 out of 5)![]() Loading...

Loading...

Kitty Wooley

September 25, 2013 at 10:42 am

Kudos, Scott. This article introduces many possibilities for better government at all levels, and not only in budget. Your graphic provides an important aid to understanding the shifts that must occur in order for employees to give their best and for government to serve the people most effectively. My personal experience in federal government has been that agency leaders haven’t yet understood how to combine hierarchical and networked forms to engage employees and raise the quality of discourse internally; most are stuck tight in old habits that have lost their vitality. You’re onto something, and I look forward to reading more of your thought here as it evolves.

B. Shine Cho

September 24, 2013 at 12:30 pm

Thank you for your intuitive article. I’m also interested in the role of budgeting as a management tool, your application of theory Y on in is very interesting.